Over the past year, the Trump administration has been laying out a clear direction for U.S. economic policy.

It shows up in the National Security Strategy, in trade actions, and in where incentives and enforcement are being applied.

I refer to this direction as a new economic Monroe Doctrine…not as a formal label, but as a useful way to describe what’s happening in practice.

Trade and capital are being organized, deliberately, into four buckets:

- Tier 1… Western Hemisphere partners

- Tier 2…Strategic allies

- Tier 3…Countries kept at arm’s length

- Tier 4…Partners losing priority

For a while, these buckets were flexible. Companies could still move between them.

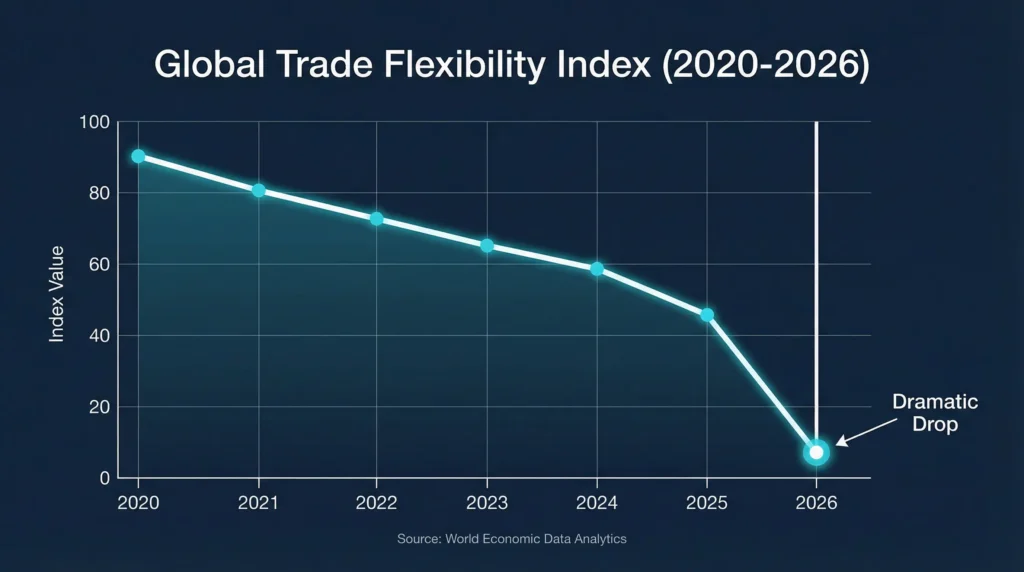

In 2026, that flexibility runs out.

The buckets harden. The system settles.

Trade Used to Bend. Now It Locks In.

For decades, global trade worked because it was flexible.

If one country got expensive, you shifted. If politics flared up, you waited it out. If a route broke, you found another.

That flexibility is mostly gone.

Risk isn’t temporary anymore. Tariffs don’t roll off. Rules stack instead of resetting.

When uncertainty lasts long enough, companies stop optimizing. They start locking in.

For operators, this means decisions that used to be reversible now shape the next decade.

Tier 1: The Western Hemisphere Gets Locked In

Tier 1 is the U.S., Mexico, Canada, and aligned partners in the Americas.

This bucket isn’t about cost. It’s about control.

Starting January 1, 2026, Mexico’s tariffs on Chinese goods routed through its borders jump as high as 50% in key categories. These are written into law. They don’t fade quietly and they aren’t easy to undo.

That one move does a lot:

- It shuts down China‑to‑Mexico arbitrage

- It forces production to stay inside the hemisphere

- It makes factory location a long‑term bet

Once production moves here, it doesn’t float back out.

A bad plant decision isn’t a margin hit anymore. It’s a multi‑year problem.

Tier 2: Allies You Can’t Replace

Tier 2 includes countries like Japan and South Korea.

They aren’t cheap. They aren’t frictionless.

But they matter.

These relationships hold because the U.S. needs them…and they need access to U.S. markets, capital, and security.

That’s why Japanese and Korean firms are putting serious money into U.S. production. These investments aren’t trials. They’re commitments.

Once that capital is down, the supply chains follow.

Tier 2 relationships get stickier… and less forgiving. Alignment matters more than price.

Tier 3: The Penalty Box (China)

China isn’t being kicked out of global trade.

It’s being sent to the penalty box.

In the penalty box, the game doesn’t stop. The player can still skate. The team can still score.

But everything gets harder.

That’s what Tier 3 looks like.

Goods still ship from China. Factories still run. Orders still get filled.

But every step costs more and takes longer.

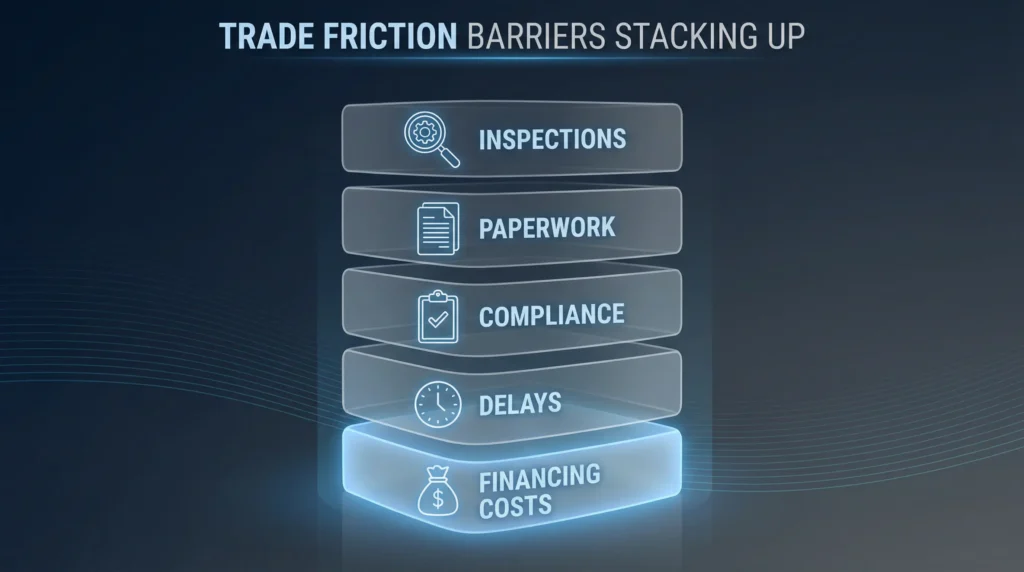

What the Penalty Box Actually Means

From the outside, trade with China can still look normal.

Inside the system, friction builds:

- More reviews and inspections

- More paperwork and compliance

- Longer approval timelines

- Higher financing costs

- Less tolerance for mistakes

None of these stop trade on their own.

Together, they compress margin and consume management attention.

Why Volume Can Hold While Risk Increases

The penalty box doesn’t always reduce volume.

It changes who carries the risk.

Inventory sits longer. Cash stays tied up. Financing becomes less predictable.

You can still source from China…but more of the downside shifts onto the buyer.

For well‑capitalized firms, that’s manageable.

For others, it isn’t.

A Risk That Rarely Gets Modeled

The penalty‑box model assumes the system keeps operating.

A kinetic conflict breaks that assumption.

This isn’t about forecasting events. It’s about understanding discontinuity risk.

In a true conflict scenario, challenges show up fast:

- Border controls tighten or close

- Payments and settlements become uncertain

- Insurance coverage gets questioned

- Employees and contractors are suddenly exposed

- Customers and shareholders want answers immediately

The issue isn’t whether trade eventually resumes.

It’s whether your business can function while it doesn’t.

The Practical Question

China remains workable for many companies.

The question is concentration, not participation.

If a large share of your revenue, supply, or workforce depends on one jurisdiction, the downside isn’t gradual.

It’s binary.

Bottom Line

The penalty box doesn’t end the game.

But heavy exposure there means accepting a category of risk that doesn’t show up in normal planning cycles.

That’s what Tier 3 actually means in 2026.

Tier 4: Partners That Lose Priority (Europe)

Europe isn’t blocked from trade.

It just loses priority.

Tier 4 worked when trade was loose and trust was high. It doesn’t work well in a system built around control and enforcement.

Nothing dramatic happens:

- More paperwork

- Longer lead times

- Higher compliance costs

No announcement. No clean break.

Just steady drag.

If your supply chain runs through Europe, expect more friction and fewer shortcuts every year.

Why Capital Matters More Than Logistics

People still focus on shipping and transportation.

That’s not the real bottleneck anymore.

The bottleneck is capital.

This system favors companies that can:

- Fund higher inventory

- Absorb delays

- Commit money for longer periods

Companies with strong balance sheets adjust. Everyone else gets squeezed.

Speed matters less than staying funded.

Why Policy Isn’t Random Anymore

Many companies still treat trade policy like noise.

That’s a mistake.

Even when courts step in or rules get challenged, the system doesn’t rewind. Claims drag on. Capital stays put. Factories don’t move back.

The details change. The direction doesn’t.

The real risk isn’t volatility. It’s misalignment.

What 2026 Actually Means

2026 isn’t a transition year.

It’s the year flexibility runs out.

The four buckets don’t disappear. They solidify.

Trade keeps moving. Goods keep shipping.

But the room to maneuver shrinks.

From here on out, supply chains don’t bend… they either hold or they break.

Bottom Line

People are still arguing about policy.

The administration has already set direction. Capital has already adjusted.

That’s what the new Monroe Doctrine reflects…and why 2026 matters.

What Comes Next

This piece is the framework.

The articles that follow will be practical.

I’ll break this down by role:

- Manufacturers: What changes when plant location, supplier choice, and capital commitments stop being reversible.

- Distributors and wholesalers: How inventory, working capital, and customer expectations shift when flexibility disappears.

- Logistics intermediaries: What happens when logistics stops being the bottleneck… and financing, compliance, and alignment take its place.

No forecasts. No politics. Just how the system actually behaves once the buckets harden.

If you operate inside these flows, stay tuned.

The easy years are over. The navigable ones are just beginning

I help companies small and large on mitigating tariff exposure and broader supply chain strategies…taking actionable steps to give you greater confidence on a logical path forward.

See Previous Articles….

https://supplychainalytics.ai/blog

Book a call….

https://supplychainalytics.ai/contact

Sign up for my newsletter…

https://supplychainalytics.ai/blog/#newsletter

Tariff Refund‑Rights Preservation Checklist

I built a one‑page checklist covering:

• Liquidation tracking • PSC timing • protest rules • documentation for scrutiny • transfer pricing alignment • weekly broker review • economic‑burden proof requirements

Download here: https://supplychainalytics.ai/refund-rights-preservation-checklist/