Tariffs Were Not About Revenue

For decades, U.S. trade policy operated under a hopeful assumption: that global markets would eventually converge around shared rules, open access, and mutual benefit.

That assumption no longer holds.

Many major trading partners:

- Subsidize domestic champions

- Restrict market access

- Manipulate currency

- Coerce technology transfer

- Ignore labor, environmental, or IP standards

That isn’t free trade. It’s asymmetric trade.

And that asymmetry is precisely why the administration stopped treating every trading partner the same.

That framing raises an uncomfortable but necessary question: should we care more about other countries being upset with what we’re doing…or about whether the policy actually works? Much of the criticism focused on tone, retaliation, and diplomatic friction, as if disapproval itself were proof of failure. But trade policy isn’t a popularity contest. In an asymmetric system, pushback is often the signal that leverage is being applied…not that it’s being misused.

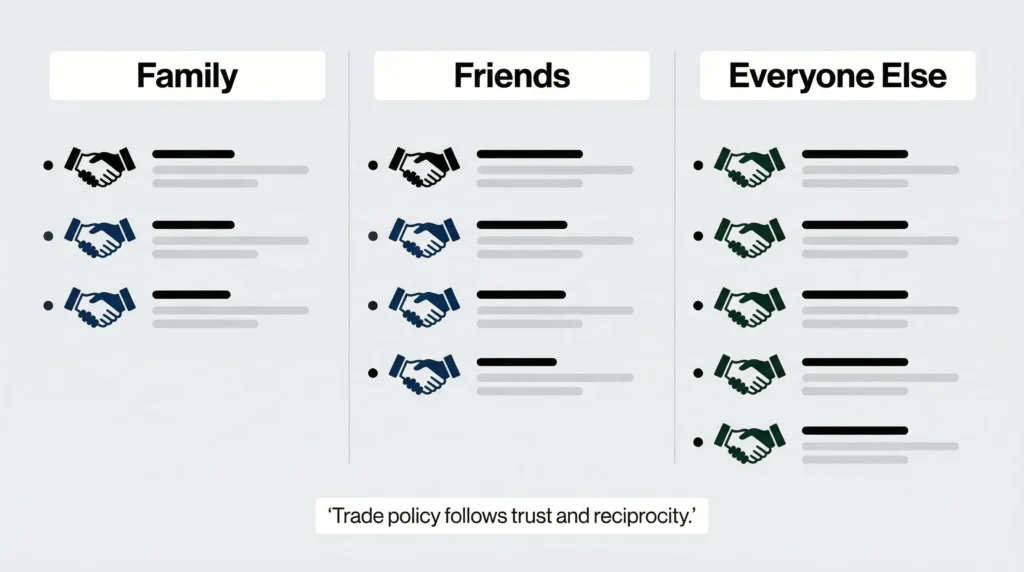

The three buckets

Countries were effectively sorted into three categories:

Family…nations with deep alignment, shared risk, and mutual dependence

Friends…partners with overlapping interests but limited strategic trust

Everyone else…countries where trade is transactional, leverage matters, and assumptions of goodwill don’t apply

Trade policy followed accordingly.

This wasn’t about isolation. It was about differentiation…recognizing that not every counterparty deserves identical access, tolerance, or trust.

A sharper reality: a modern Monroe Doctrine

Under Trump’s National Security Strategy, this framework amounted to what is best described as a modern, informal Monroe Doctrine.

Not territorial. Not imperial.

But economic and strategic.

The signal was unmistakable: the United States would no longer organize trade policy around global neutrality, but around spheres of trust, dependence, and risk.

Near‑shoring, friend‑shoring, and hemispheric resilience weren’t slogans…they were boundary lines.

Access to the U.S. market would increasingly reflect alignment, reciprocity, and strategic reliability, not just WTO formality.

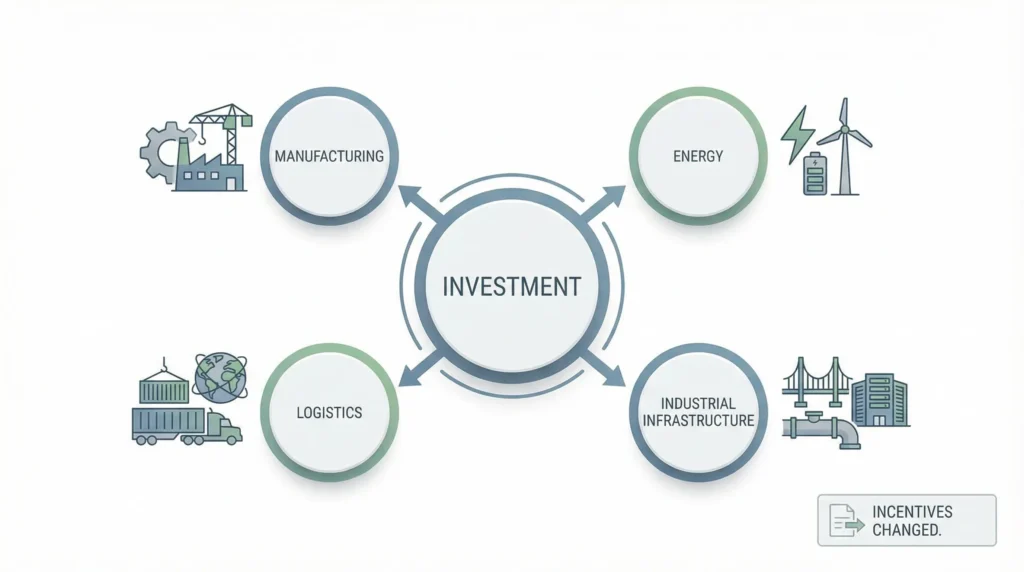

Follow the capital, not the commentary

One of the least discussed outcomes of tariffs has been direct foreign investment. If the current tote board is in the trillions of dollars that is a good thing.

Rather than capital fleeing:

- Investment is flowing into North America

- Manufacturing capacity relocated closer to end markets

- Energy, logistics, and industrial infrastructure expanded

- Supply chains shortened and diversified

Capital doesn’t move because of opinion pieces. It moves when incentives change.

Tariffs changed incentives.

Trade deficits actually matter

The U.S. trade deficit is often waved away as an accounting curiosity — a harmless byproduct of consumption or dollar strength.

I once heard an executive say they had a “trade deficit” with the local grocery store. They meant it half‑jokingly, but it stuck with me…because anecdotes like that have a way of framing complex issues as no big deal. I’m sure part of what they were really thinking was, why can’t we just go back to free trade…back to the way things were?

A household running a deficit with its grocery store isn’t really trading; it’s just consuming.

At the national level, persistent trade deficits mean something very different:

- Dollars leaving the domestic system

- Financing flowing outward

- Productive capacity relocating

- Strategic leverage accumulating elsewhere

When those dollars flow to countries that do not share our interests, the risks compound quietly over time.

Reducing that dynamic to a casual analogy makes it feel harmless and short‑term…when it’s anything but.

Deficits aren’t immoral. They’re not automatically fatal.

But pretending they’re meaningless because “we get stuff” ignores the strategic reality of who controls production, capital, and leverage over time.

That’s the distinction many debates miss.

The dollar’s privilege isn’t permanent

The U.S. dollar remains the world’s reserve currency…but that status rests on:

- Stability

- Trust

- Productive capacity

- Strategic credibility

Some view this moment as part of a broader global economic reset, where trade realignment, supply‑chain restructuring, and currency influence are all moving pieces of the same board. In that context, reserve‑currency status isn’t just a benefit…it’s the endgame variable. Few would argue that losing it wouldn’t fundamentally change the country’s economic position. If that privilege goes away, it’s not a policy setback…it’s game over.

Tariffs were one tool…not the only one…used to slow that erosion and buy time.

The Chaos Everyone Fixated On

If you listened only to short‑term commentary, the early months(and even still) after tariffs took effect sounded apocalyptic.

“Chaos.” “Disruption.” “Proof this couldn’t work.” Trust me I have heard so many I can’t list them all…

Those descriptions weren’t entirely wrong.

They were just mistaken for conclusions instead of symptoms.

There’s no question 2025 was chaotic…and for some importers, outright catastrophic. Sudden cost spikes, contract disputes, delayed shipments, broken assumptions around lead times, margin compression, abandoned cargo, and forced write‑offs hit hard. Businesses that supported importers…logistics providers, distributors, customs brokers, finance teams, and downstream service firms…felt the shock just as acutely. For many, it wasn’t an abstract policy debate; it was a year of triage, restructuring, and, in some cases, failure.

What’s often missed is that this pain wasn’t evidence the policy “didn’t work.” It was evidence that the system was being forced to change…even though, for many firms, the bad clearly outweighed the good in the short term.

Inflation…what actually happened

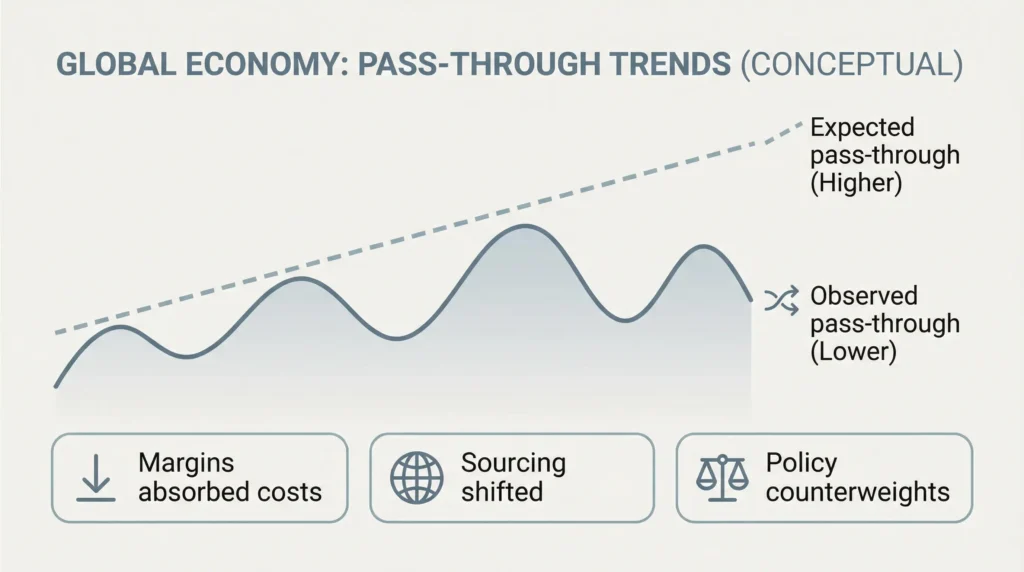

Inflation was always the sharpest critique of tariffs…and the one delivered with the most confidence.

Prices would spike. Consumers would pay. The damage would be obvious and unavoidable.

But as 2025 unfolded, that narrative softened.

Across economists, central bank commentary, sell‑side research, and industry surveys, a consistent pattern emerged: the pass‑through from tariffs to consumer prices was smaller, slower, and more uneven than predicted. Costs showed up in pockets, were absorbed in margins, or were offset through sourcing shifts and pricing adjustments.

That outcome wasn’t accidental.

Over the same period, government actions worked against inflationary pressure: tighter financial conditions, slower discretionary spending growth, inventory normalization, energy price stabilization, targeted supply‑side incentives, further de-regulation, all helped blunt price increases. None of these eliminated costs…but together they reduced the odds of a clean, tariff‑driven inflation spike.

There’s also a harder truth that rarely gets acknowledged.

Companies that didn’t survive never passed higher prices on.

Firms that failed during the transition didn’t raise prices…they exited. Their disappearance dampened measured inflation while masking real economic pain underneath. Price stability, in that sense, reflected not just absorption and adjustment, but attrition.

Some have argued inflation was simply delayed…that it would arrive in early 2026 once inventories cleared and contracts reset.

The theory was tidy. Reality wasn’t.

Supply chain lead times didn’t operate in isolation. Over that same period, firms renegotiated suppliers, simplified product lines, shifted sourcing, reworked logistics, and selectively repriced where demand allowed. The broader environment shifted as well.

For a clean inflation spike to suddenly appear on schedule, businesses and policymakers would have had to do nothing.

They didn’t.

And it’s worth saying: it’s still early 2026. Some effects may yet surface, and the full adjustment isn’t finished. But inflation outcomes so far reflect adaptation, policy counterweights, and firm‑level selection…not a simple tariff‑equals‑prices story.

That’s why clean, calendar‑based inflation predictions tend to disappoint.

Where the Glass Was Half Full

None of the chaos of 2025 should be minimized. But disruption does sometimes force changes that stability never would.

One of the clearest outcomes was optionality. Firms that had relied on single‑country or single‑supplier models were forced to build alternatives — secondary suppliers, regional backups, flexible logistics routes, and contingency pricing structures. Those options weren’t cheap, but they mattered.

The second was resilience. Supply chains became less optimized for cost alone and more tolerant of shocks. Inventory strategies shifted. Contracts changed. Risk was priced explicitly instead of being assumed away.

Optionality doesn’t eliminate disruption. Resilience doesn’t prevent future shocks.

But together, they reduce fragility — and that matters in a world where geopolitical, energy, and financial disruptions are no longer rare events.

That may not show up cleanly in quarterly data. But it changes how the system absorbs stress over time.

The real takeaway

Tariffs weren’t free. They weren’t clean. They weren’t painless.

But they were also not about revenue.

They were a geopolitical tool used in a world where:

- Not everyone is a friend

- Not all trade is fair

- Deficits matter

- Economics and power are inseparable

For those still arguing 2025 as a clean win or loss, that certainty is the problem. Revenue, inflation, and chaos were never meant to be scorecards — and treating them as such ensured the debate missed what actually changed.

I help companies small and large on mitigating tariff exposure and broader supply chain strategies…taking actionable steps to give you greater confidence on a logical path forward.

Book a call….

https://supplychainalytics.ai/contact

Tariff Refund‑Rights Preservation Checklist

I built a one‑page checklist covering:

• Liquidation tracking • PSC timing • protest rules • documentation for scrutiny • transfer pricing alignment • weekly broker review • economic‑burden proof requirements

Download here: https://supplychainalytics.ai/refund-rights-preservation-checklist/