Recent proceedings before the Court of International Trade have focused attention on potential refunds of tariffs imposed under the International Emergency Economic Powers Act (IEEPA). While the legal developments have generated understandable interest, the more immediate issue for most companies is operational readiness.

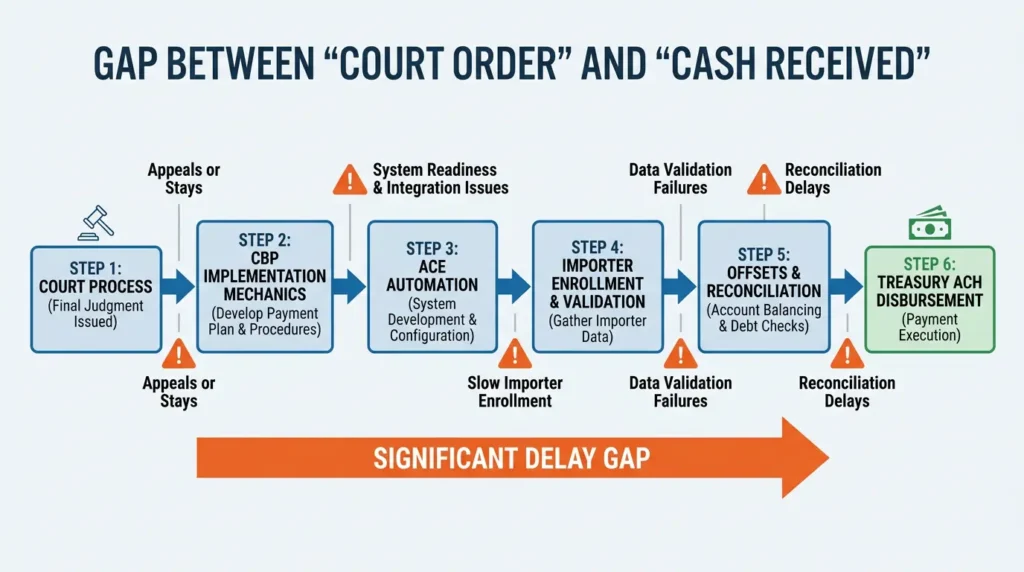

At this stage, nothing is final in a practical sense. The Court of International Trade continues to determine the procedural framework and implementation timeline. Further appeals remain possible. Stays can be requested. Implementation mechanics can be clarified, modified, or slowed. Court scheduling does not automatically translate into Treasury disbursement.

CBP has indicated that automated refund functionality within the Automated Commercial Environment could be operational within approximately 45 days. Even if that timeline ultimately shifts, it creates a near‑term execution horizon that companies should plan against.

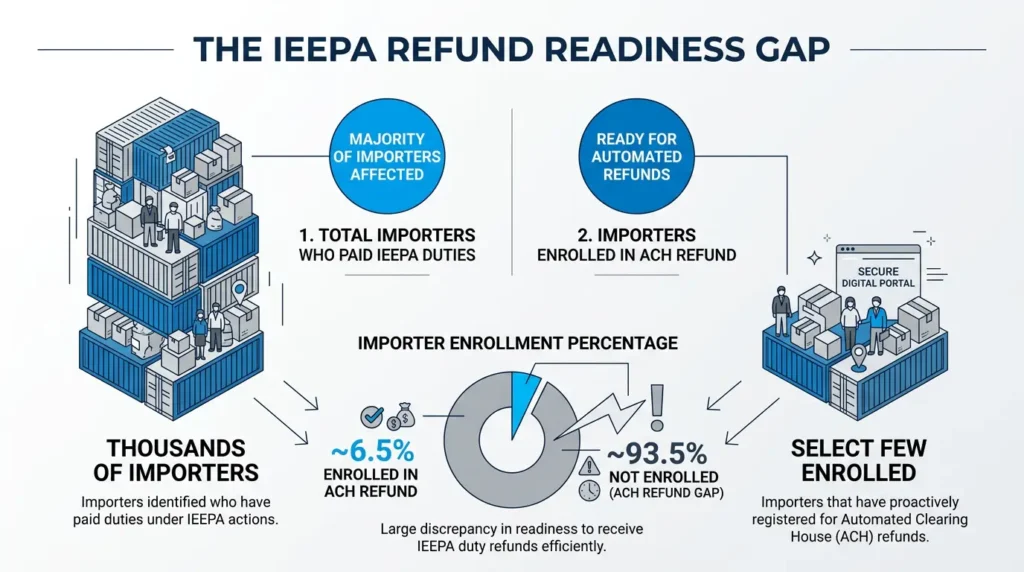

As of March 4, 2026:

- 330,566 importers had paid IEEPA duties

- 21,423 importers were enrolled in ACH Refund

That equates to approximately 6.5 percent of affected importers enrolled to receive electronic refunds, or 93.5 percent not yet operationally positioned to receive disbursement if refunds got switched on today….

The readiness gap is significant.

The Court Order and Procedural Posture

The Court has ordered CBP to:

- Liquidate all unliquidated entries without IEEPA duties, and

- Reliquidate liquidated entries for which liquidation is not yet final, removing IEEPA duties.

This distinction is critical.

Entries that are not final remain within the Court’s corrective reach. Entries that are already final….generally meaning the 180‑day protest window has expired…are not clearly subject to automatic reliquidation under the current order and remain the most legally sensitive category.

Implementation remains subject to procedural posture and any appellate activity.

A judicial ruling does not automatically produce payment. There is a structural gap between court direction and system execution. The Court determines process. CBP implements mechanics and can comply quickly if able or drag out disbursements through several means.

Further motions, clarification orders, or appeals may affect timing. Companies should assume the process remains dynamic.

What CBP Represented Regarding Scale

CBP referenced approximately 53,173,939 entry‑specific refunds. Manual processing was estimated to require approximately 4.4 million staff hours. Automation is intended to consolidate and streamline this volume.

The proposed workflow includes:

- Importer declaration through ACE

- Automated recalculation of duties and interest

- Validation against outstanding debts

- Aggregation by importer and liquidation date

- Treasury issuance via ACH

Even with automation, enrollment, validation checks, and internal reconciliation will determine how quickly funds are actually received.

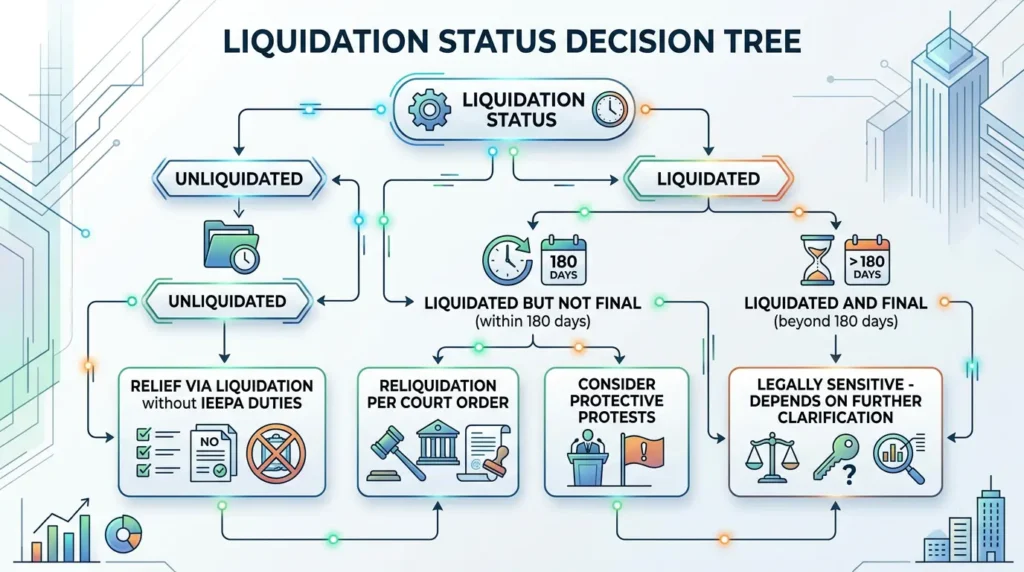

Liquidation Status Is the Dividing Line

The most important technical variable is liquidation status.

Unliquidated (Pre‑Liquidation) Entries

If entries remain unliquidated:

- Duties are not yet final.

- The Court has directed liquidation without IEEPA duties.

- No protest is required.

Relief for these entries flows through the liquidation process.

Liquidated Entries That Are Not Final

If an entry has liquidated but remains within the 180‑day protest period:

- The Court has ordered reliquidation without IEEPA duties.

- These entries remain legally non‑final.

- Protective protests may still be considered as a preservation measure depending on company risk tolerance.

Liquidated and Final Entries

If more than 180 days have passed since liquidation:

- Entries are generally final under 19 U.S.C. § 1514.

- Protest rights are extinguished.

- The current order does not clearly compel automatic reliquidation of these final entries.

These entries represent the greatest legal uncertainty and depend on further court clarification or appellate developments.

Are Companies Likely to File New Lawsuits?

Based on the recent ruling and its nationwide structure, it is not likely that companies will continue filing new lawsuits simply to preserve rights.

Where a lead case is already before the Court and relief extends broadly to non‑final entries, duplicative litigation becomes less necessary. The more immediate focus is liquidation posture and protest timing, not a new wave of independent filings.

The dividing line is not whether to sue. It is whether entries are unliquidated, non‑final, or administratively final. Legal viewpoints continue to evolve on this issue over the last few weeks.

Where the Risk Now Sits

Three practical risk areas are emerging.

1. Timing Risk

Automation could be operational within approximately 45 days. However, only about 6.5 percent of affected importers were enrolled in ACH Refund as of early March 2026. Even if the system is ready, companies not enrolled will experience delay.

2. Validation and Offset Risk

Refund amounts will be recalculated prior to issuance. The process includes validation checks and potential offsets for outstanding debts. Companies should anticipate reconciliation rather than mechanical repayment.

3. Data Integrity Risk

Refund submissions consolidate historical entry data. Companies should audit:

- HTS classifications used during the IEEPA period

- Valuation methodology consistency

- Origin documentation sufficiency

- Entry‑level reconciliation

Preparation reduces both timing uncertainty and validation exposure.

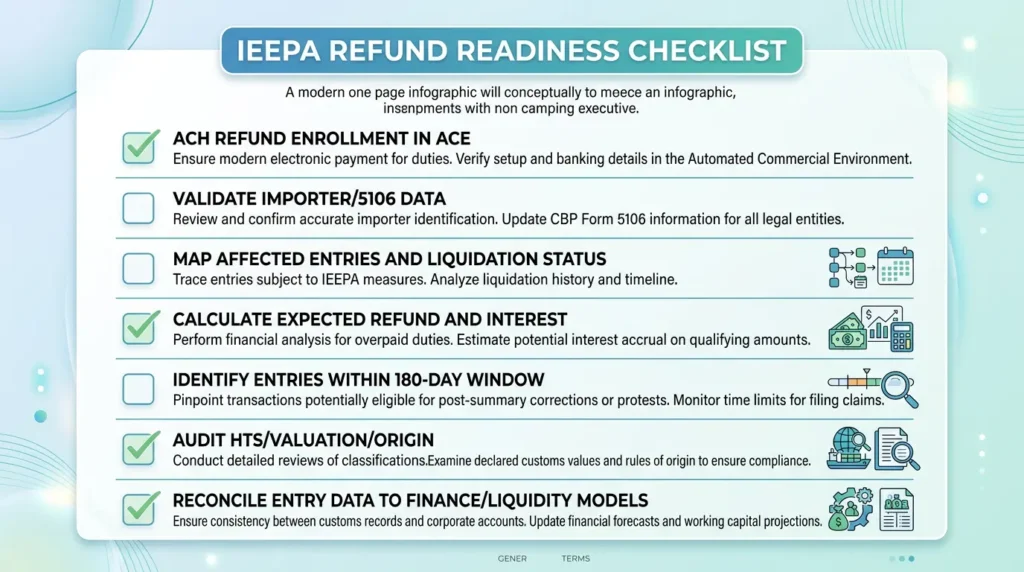

What Companies Should Be Doing Now

The following actions are independent of any particular court date:

- Confirm ACH Refund enrollment within ACE

- Validate importer account and 5106 data

- Identify all affected entries and confirm liquidation status

- Independently calculate expected refund and interest

- Evaluate whether any entries fall within the 180‑day protest window

- Audit classification, valuation, and origin positions

- Reconcile entry data to financial reporting and liquidity models

These are readiness steps, not litigation reactions. This is a line by line process…no shortcuts.

Bottom Line

As of early March 2026:

- Over 330,000 importers paid IEEPA duties

- Approximately 6.5 percent were enrolled to receive ACH refunds

- Roughly 93.5 percent were not operationally positioned

- Approximately 53 million entry‑specific refunds are implicated

- The Court has ordered liquidation or reliquidation of non‑final entries without IEEPA duties

- Fully final entries remain legally sensitive

- Automation could be operational within roughly 45 days

- Implementation remains subject to Court process and potential appeal

- March 17, 2026 is a procedural court date and does not alter the operational steps companies should already be taking

Refund mechanics are real. Execution risk is measurable. Timing remains contingent.

Companies that move now on data gathering, entry audits, enrollment validation, and liquidation mapping will be positioned to act when the legal and operational tracks converge.

This article is based on publicly available information and court representations as of early March 2026. It is provided for informational purposes only and is not intended as legal, financial, or tax advice.