Here is what nobody told you over the weekend: a dissenting Supreme Court justice handed the administration a legal roadmap to tariffs higher than anything imposed under IEEPA…with no expiration date, no 150-day clock, and a rate ceiling of 50 percent.

It’s called Section 338. It’s been sitting in the Tariff Act of 1930 for 96 years without ever being fired. That streak may be ending.

I understand the impulse to celebrate. The IEEPA ruling was a genuine legal milestone…the Court drew a real line. But in my work with manufacturers and distributors, premature relief is its own risk. Companies that exhaled in 2019 after the first round of China tariffs, exhaled again after COVID disruptions, exhaled again after the first IEEPA challenges…those same companies tend to be the ones scrambling when the next move comes. The ones who didn’t exhale are better positioned today.

So before you brief the board on what Friday’s ruling means, read the dissent.

Justice Brett Kavanaugh voted to uphold IEEPA… he lost that argument 6-3. But in explaining his dissent, he did something that may prove more consequential than the majority opinion itself. He listed the alternative authorities available to the president, verbatim:

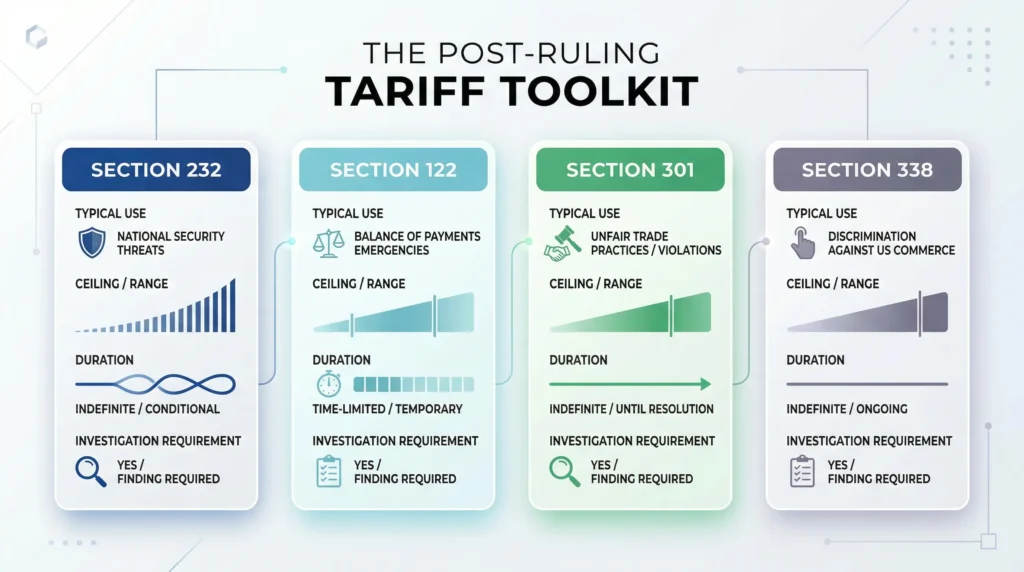

“Those statutes include, for example, the Trade Expansion Act of 1962 (Section 232); the Trade Act of 1974 (Sections 122, 201, and 301); and the Tariff Act of 1930 (Section 338). In essence, the Court today concludes that the President checked the wrong statutory box.”

Checked the wrong box. Kavanaugh wasn’t saying the tariffs were wrong…he was saying the administration used the wrong legal vehicle. The destination was fine. Just take a different road.

Trump read that passage aloud at the press conference. He called Kavanaugh a genius. Trade counsel across the country opened their copies of the Tariff Act of 1930 the same afternoon.

Don’t Skip Section 122

Before we get to Section 338, let’s talk about the bridge nobody should be dismissing.

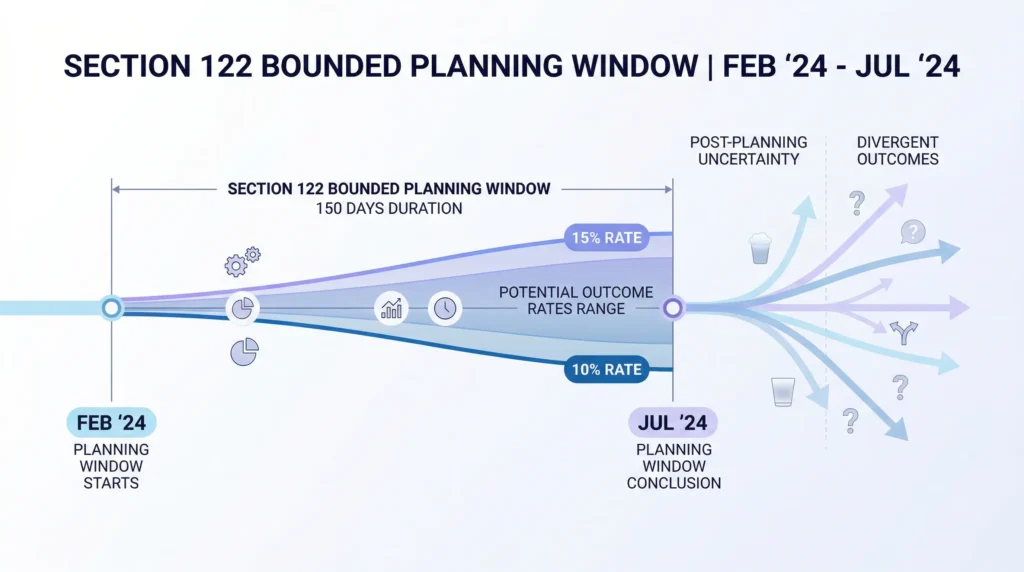

The administration signed at 10% Friday evening. By Saturday, Trump was on social media announcing he would push it to the statutory maximum of 15%…before the legal paperwork was ready. As of February 24th, when tariffs went live, CBP confirmed collection at 10%. A second proclamation raising it to 15% is being prepared. The administration has made clear there is no change of heart on the higher rate. For planning purposes, model at 15%. That is the stated destination and the statutory ceiling.

More importantly: don’t dismiss Section 122 because it feels temporary. In a lot of boardrooms it’s being written off as a placeholder. A speed bump. Something to manage through while waiting for the real outcome.

That is a mistake.

Section 122 is the only moment of genuine rate certainty in the entire post-ruling environment. Ten or fifteen percent…either way, it is known, bounded, and legally straightforward relative to what comes next. The companies treating it as background noise are the same companies that will be scrambling when the rate environment shifts again in July…or before.

The smart play is to model your supply chain economics against Section 122 right now. Not because it’s permanent. It isn’t. But because it’s the floor you can actually see, and what comes after it…Section 301 investigations maturing in nine months, Section 338 waiting in the toolkit with a 50 percent ceiling…may not give you the same visibility. Use the 150-day window as a planning baseline, not a waiting room.

The companies that fared best through the IEEPA period were not the ones who predicted the outcome most accurately. They were the ones who maintained optionality at each inflection point. Section 122 is an inflection point. Treat it like one.

The Road Nobody Has Taken in 96 Years

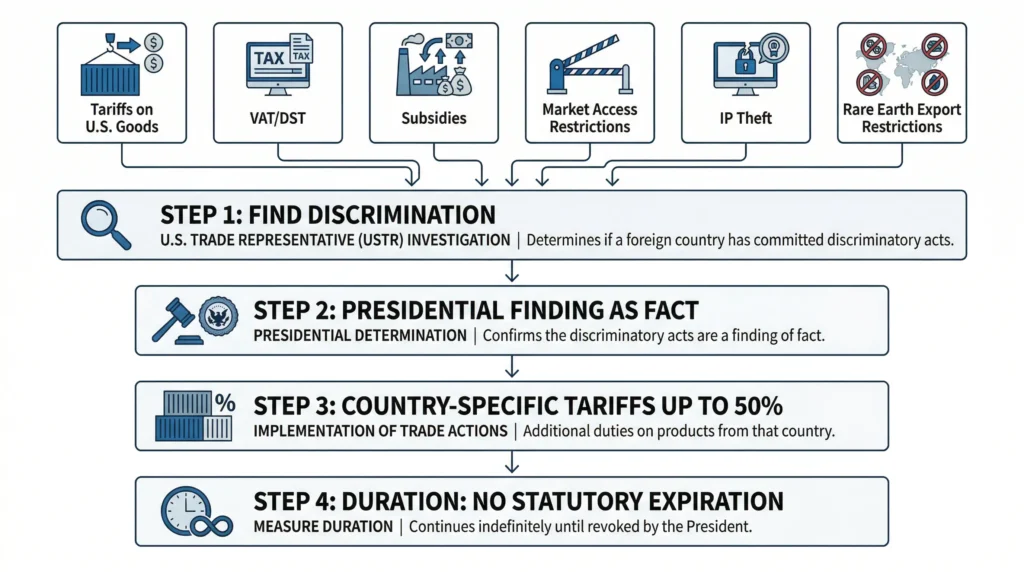

Section 338 of the Tariff Act of 1930 authorizes the president to impose tariffs of up to 50 percent ad valorem on imports from any country that “discriminates” against U.S. commerce. The president invokes it whenever he “finds as a fact” that such discrimination exists. No formal agency investigation required. No statutory expiration. No 150-day clock requiring a Congressional vote four months before midterms.

That context matters. Section 338 was written into the Smoot-Hawley Tariff Act…the same legislation economists point to as the policy that turned a financial crisis into the Great Depression. Congress in 1930 was building the most protectionist tariff wall in American history, and even then, Section 338 was considered the weapon of last resort. The United States threatened to invoke it against France in 1932. Considered it against Japan in the late 1930s. Neither time did an administration follow through. For nearly a century, Section 338 sat in the statute books as a deterrent…something you pointed at but never fired.

In September…months before the Supreme Court ruling…Treasury Secretary Bessent told Reuters the administration was already considering Section 338 as an explicit contingency if IEEPA fell. This was not improvisation on a bad Friday afternoon. It was contingency planning. By the time Trump stood at the podium and read Kavanaugh’s dissent aloud, the administration already knew which road it was taking next.

What “Discrimination” Means…And Why That’s the Whole Ballgame

The statute doesn’t define discrimination with any precision. That vagueness kept it dormant for nearly a century. It is now the administration’s greatest asset.

The president could find that any country maintaining tariffs on American goods is discriminating against U.S. commerce. He could find that digital services taxes discriminate. That VAT structures discriminate. That state subsidies, market access restrictions, or currency practices discriminate.

And then there is intellectual property theft.

This is where Section 338’s vague discrimination standard becomes a genuinely powerful instrument…particularly against China, but not only China. State-sponsored theft of American trade secrets, forced technology transfer as a condition of market access, systematic counterfeiting of U.S. products, patent infringement embedded in industrial policy…all of it fits comfortably within a broad reading of “discrimination against U.S. commerce.”

The administration has already used IP theft as the legal foundation for its China tariff architecture. The entire Section 301 China tariff regime…still in force, untouched by the IEEPA ruling…was built on a 2017 investigation into forced technology transfer, IP theft, and innovation suppression. The government has already made the factual record. It has already identified the behavior. It has already called it discriminatory under a different statute.

If the administration finds…as it plausibly could…that a country’s systematic theft of American intellectual property constitutes discrimination against U.S. commerce, it has a statutory argument for 50 percent tariffs that did not exist under IEEPA and does not expire in 150 days. That is not a speculative reading. It is the plain language of the statute applied to documented behavior that the U.S. government has formally identified, investigated, and acted on under another authority. The factual predicate is already in the record.

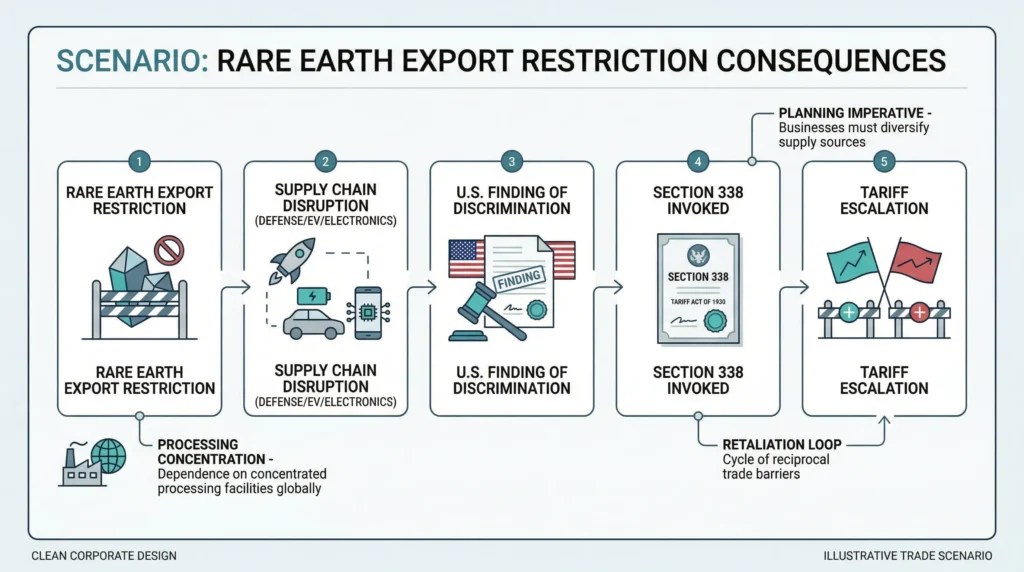

And then there is the scenario that may actually pull the trigger on Section 338…rare earths.

China controls roughly 90 percent of global rare earth processing. These are the materials inside electric motors, defense systems, semiconductors, wind turbines, and virtually every advanced technology product the U.S. either manufactures or depends on. China has already used export restrictions on rare earths as a retaliatory weapon…most recently in April 2025, explicitly tied to U.S. tariff actions. When China restricts rare earth exports in response to American trade policy, it is not environmental stewardship. It is economic coercion targeted specifically at U.S. commerce.

Here is what most people have missed: the U.S. government already has a WTO-adjudicated finding that China’s rare earth export controls are discriminatory. In 2014, a WTO panel ruled that China’s restrictions created arbitrary and unjustifiable discrimination between countries and served as “a kind of consumption assurance” for China’s domestic industries…not conservation. The U.S. won that case. The WTO Appellate Body upheld it. China dropped the quotas in 2015…and then rebuilt the same architecture through export licensing and deny lists, achieving the same result through a different mechanism.

Under Section 338, the president needs to “find as a fact” that discrimination exists. The WTO already found it. The U.S. government was the one arguing the case. That factual predicate isn’t being constructed from scratch…it’s sitting in a decade-old adjudicated record, updated by China’s own 2025 conduct.

If China restricts rare earth exports again in response to Section 122 or Section 338 pressure, the administration has a near-perfect legal fact pattern for invoking Section 338 in return…country-specific, documented, WTO-condemned discrimination against U.S. commerce, deployed as explicit economic retaliation. That is not a hypothetical. It is the most likely tripwire that gets this statute actually used for the first time in 96 years.

Supply chain executives with rare earth exposure…in defense, EV, electronics, or advanced manufacturing…should be war-gaming this scenario now, not after the export license denials start arriving.

The International Trade Commission has a role in the statute…it is directed to inform the president when discrimination is occurring…but whether that function is a prerequisite or merely advisory has never been litigated. The Congressional Research Service has concluded Section 338 falls in the category of statutes that do not require a formal agency finding before the president can act. That interpretation has never been tested in court…which means the administration could invoke Section 338 before a court gets the chance to weigh in.

The Rate Math Nobody Is Running

Under Section 122: 15 percent ceiling. Statutory maximum. Full stop.

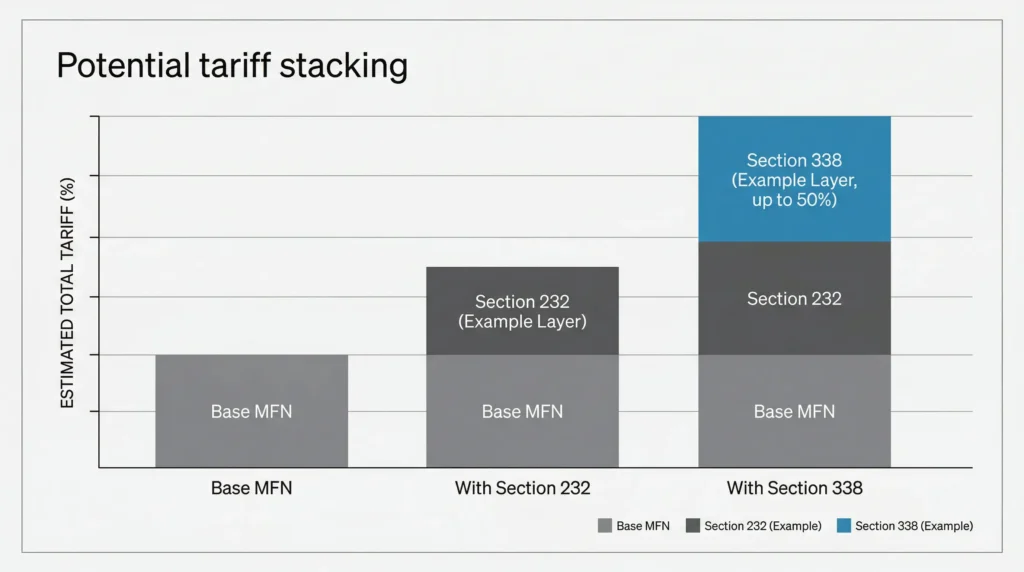

Under Section 338: 50 percent ad valorem. And because the statute authorizes “new and additional” duties, there is a credible argument that Section 338 tariffs stack on top of existing MFN rates and Section 232 tariffs already in place.

Consider what that looks like on the ground. A steel product currently faces a 25 percent Section 232 tariff stacked on a base MFN rate. Add a Section 338 finding of discrimination against the country of origin…up to 50 percent additional…and the effective rate on that product could reach 80, 90, or higher depending on the baseline.

Pharmaceuticals are the more alarming example. The administration has publicly floated a 250 percent Section 232 proposal on drugs. If Section 338 authority is layered on top of that in a country-specific finding, the effective tariff rate on certain pharmaceutical imports would become functionally prohibitive…not a tax on trade, but a wall against it.

This is not a fringe legal theory. It is the plain reading of the statute combined with stacking logic the administration has already demonstrated it is willing to use.

The Legal Challenge Problem…And Why the Timeline Doesn’t Help You

The obvious question: doesn’t the same major questions doctrine that killed IEEPA kill Section 338?

Maybe. Eventually.

The argument for Section 338 survival is that the statute is more explicit than IEEPA…it actually uses the word “duties,” specifies a rate ceiling, and describes a triggering condition. Courts have historically required clear statutory language before applying major questions to invalidate a delegation. Section 338 has more of that language than IEEPA did.

The Peterson Institute has raised the more interesting challenge: using Section 338 to impose across-the-board tariffs against all trading partners simultaneously would look structurally similar to what IEEPA just did. A court could view it as circumventing the ruling rather than complying with it.

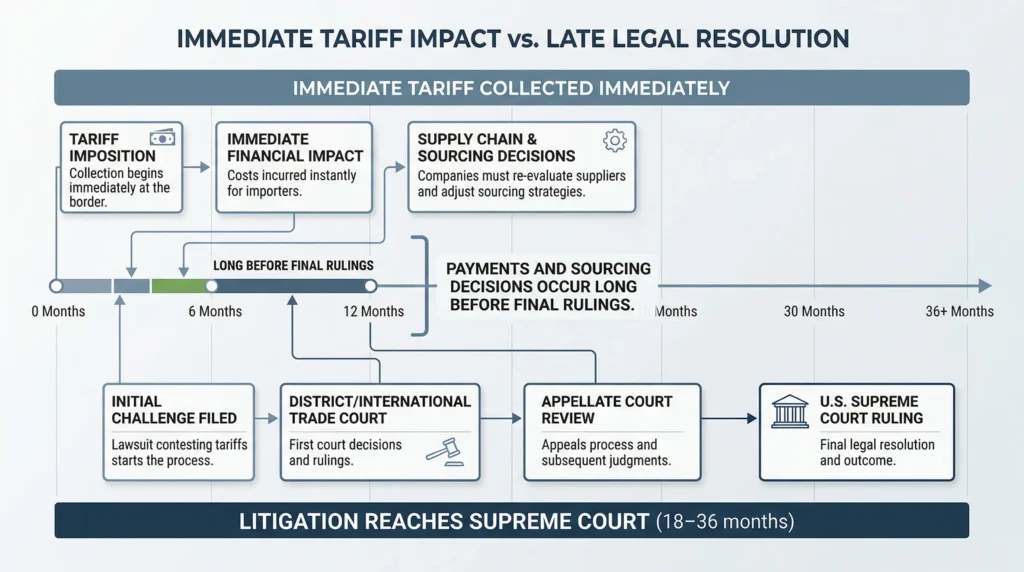

But here is the planning reality your legal team needs to absorb: that argument takes 18 to 36 months to reach the Supreme Court. Your sourcing decisions, capital allocation, and contract terms don’t wait for appellate timelines. The administration invokes. Importers pay. Litigation proceeds. Rates stay in place while the case is briefed, argued, and decided. That is exactly what happened with IEEPA…companies paid for nearly a year before the Court acted. Plan for the same dynamic here.

What Kavanaugh Actually Did…

Step back and consider what just happened in the architecture of U.S. trade law.

The majority opinion reined in one tool…a broad emergency authority that the Court said Congress never intended for tariffs. That is genuinely significant.

The dissent listed three alternative authorities, described them as sufficient to justify “most if not all” of the same tariffs, and characterized the majority’s problem as a procedural box-checking failure rather than a substantive limit on presidential power.

The administration is now checking the boxes Kavanaugh identified. Section 122 is already in place. Section 301 investigations launched February 20th. Section 232 intact and expanding. Section 338 publicly named, pre-planned by Treasury, and waiting.

Kavanaugh lost the IEEPA vote. In losing, he may have handed the administration a more durable legal architecture than IEEPA ever provided…one built on statutes with explicit rate ceilings, named triggering conditions, and nearly a century of surviving constitutional challenge.

The instrument changed. The intent didn’t. The rate ceiling under the new toolkit is higher.

The July 24 Cliff…And What Comes After

Section 122 expires July 24th. Four months before midterms. Congressional extension requires every competitive-district Republican to vote for a tax that cost the average American household over $1,300 in 2025. That vote is not happening easily, if at all.

The Section 301 investigations launched February 20th mature in approximately nine months…around November, after the expiration and after the midterms. There is a gap. It is real. It is unresolved.

Section 338 is the bridge that fills that gap without requiring Congressional approval, without an expiration date, and with a rate ceiling that makes the IEEPA period look restrained by comparison.

A dissenting justice called it a legitimate road. The administration was already planning to take it before the ruling came down.

Mid-July is closer than it looks. And for supply chain executives who think July 24th is the finish line…it may be the starting gun.

Dan Krouse is a supply chain advisor at Supplychainalytics. This article reflects factual analysis of publicly available legal and trade information and does not constitute legal or financial advice.